Ever since a group of 22 economists wrote an open letter to the Federal Reserve advocating for an increase in the inflation target, economics blogs have been abuzz with discussion about the merits of a targeting an inflation rate greater than 2%.

While I don't have much to say about the value of changing the inflation target (I pretty much agree with the authors of the letter), I do think there are several practical issues that the Fed would have to deal with if it did want to start targeting e.g. 4% PCE inflation.

As I see it there are currently two obstacles that make it practically hard for the Fed to increase its inflation target: 1) the Fed doesn't have enough credibility, and would squander what little it has if it tried, to raise inflation and 2) interest rates are so low that providing the necessary stimulus to get inflation to 4% is basically impossible in the short to medium term.

The Fed adopted a 2% inflation target in 2012 after unofficially targeting 2% inflation for years up until that point, but ironically core PCE inflation has not been 2% since March of 2012 (the headline rate was briefly 2.15% this February).

This consistent undershoot of the inflation has begun to take its toll on the Fed's credibility, with both expected inflation measured by the University of Michigan survey of Consumers and spread between normal treasury securities and inflation protected ones falling below normal levels after 2014.

Since the Fed can't even meet its own low inflation target, what makes anyone think it can meet a higher one? Before we even think about raising the inflation target, we should make sure the Fed is actually capable and willing to let inflation reach 2%. If it that doesn't happen, I'm skeptical that markets and consumers (who are probably too backward looking to expect inflation until they've been experiencing it for a while anyway) will take an increased inflation target seriously.

Since the Fed can't even meet its own low inflation target, what makes anyone think it can meet a higher one? Before we even think about raising the inflation target, we should make sure the Fed is actually capable and willing to let inflation reach 2%. If it that doesn't happen, I'm skeptical that markets and consumers (who are probably too backward looking to expect inflation until they've been experiencing it for a while anyway) will take an increased inflation target seriously.

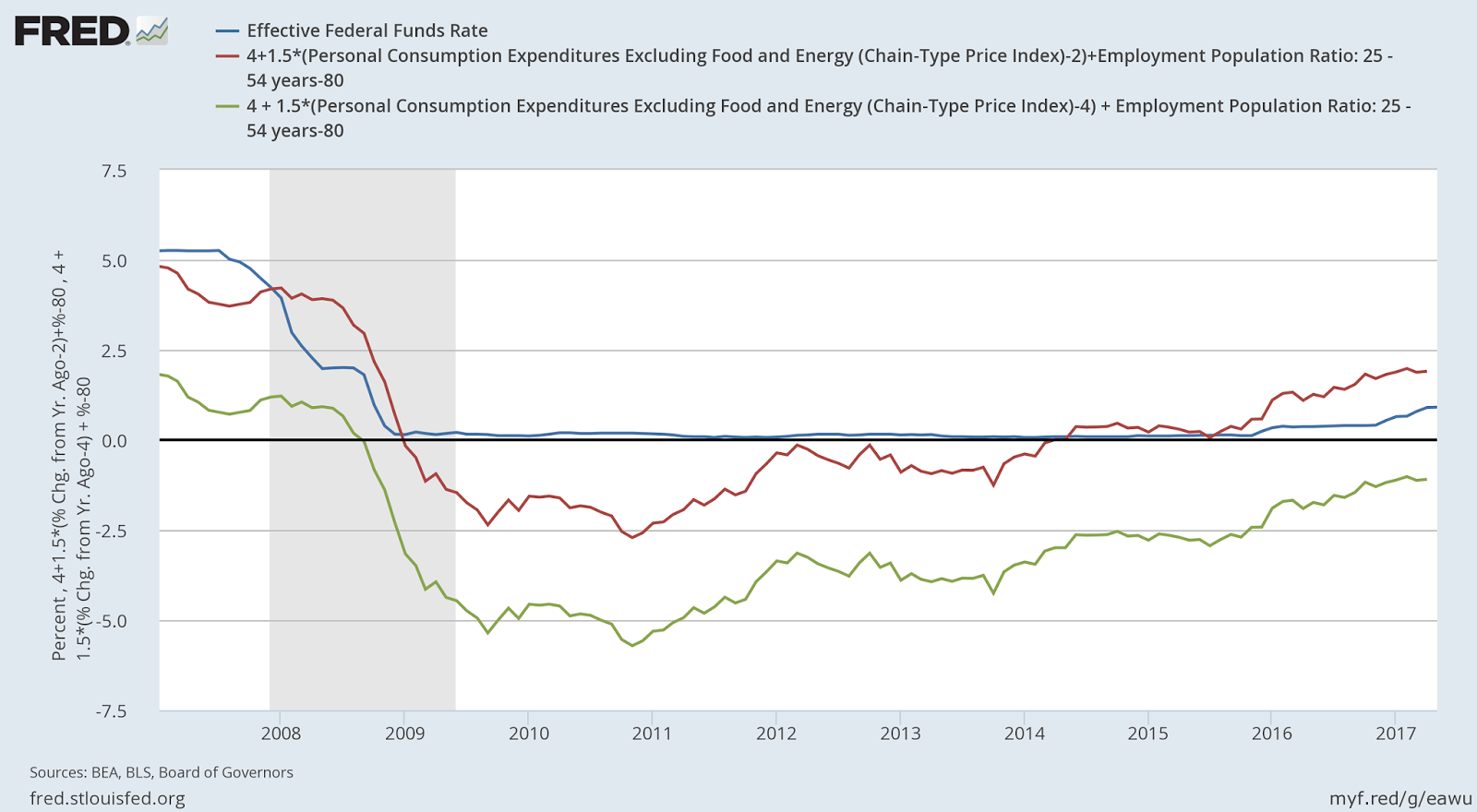

Beyond just announcing that it is now targeting a higher inflation rate, say 4%, the Fed would have to take concrete action to raise inflation to its new target. This would involve lowering interest rates considerably, because inflation would now be about 2.4% below target instead of just 0.4%. A useful way of thinking about this is comparing a Taylor Rule with a 2% inflation target and one with a 4% inflation target.

Here the blue line is the actual Federal Funds rate, while the red line is what a Taylor Rule -- with a coefficient of 1.5 on inflation and 1 on the "output gap" (in this case defined as the difference between the prime age employment rate and its "full employment" level of 80%) -- would suggest the interest rate be with a 2% inflation target. The green line shows what interest rate we should expect the Fed to set given a four percent inflation target. Basically, in order to commit to raising inflation to 4%, the Fed would have to either find a way to make interest rates significantly negative or otherwise go back to the zero lower bound for the foreseeable future.

Here the blue line is the actual Federal Funds rate, while the red line is what a Taylor Rule -- with a coefficient of 1.5 on inflation and 1 on the "output gap" (in this case defined as the difference between the prime age employment rate and its "full employment" level of 80%) -- would suggest the interest rate be with a 2% inflation target. The green line shows what interest rate we should expect the Fed to set given a four percent inflation target. Basically, in order to commit to raising inflation to 4%, the Fed would have to either find a way to make interest rates significantly negative or otherwise go back to the zero lower bound for the foreseeable future.

I know that even the people who signed the letter weren't suggesting an immediate switch to a higher inflation target, but to the extent that they want the change to happen in the next few years, during which the economic climate will probably remain about the same, it's unclear as to whether or not a quick increase in inflation is actually that possible.

While I don't have much to say about the value of changing the inflation target (I pretty much agree with the authors of the letter), I do think there are several practical issues that the Fed would have to deal with if it did want to start targeting e.g. 4% PCE inflation.

As I see it there are currently two obstacles that make it practically hard for the Fed to increase its inflation target: 1) the Fed doesn't have enough credibility, and would squander what little it has if it tried, to raise inflation and 2) interest rates are so low that providing the necessary stimulus to get inflation to 4% is basically impossible in the short to medium term.

The Fed adopted a 2% inflation target in 2012 after unofficially targeting 2% inflation for years up until that point, but ironically core PCE inflation has not been 2% since March of 2012 (the headline rate was briefly 2.15% this February).

This consistent undershoot of the inflation has begun to take its toll on the Fed's credibility, with both expected inflation measured by the University of Michigan survey of Consumers and spread between normal treasury securities and inflation protected ones falling below normal levels after 2014.

Beyond just announcing that it is now targeting a higher inflation rate, say 4%, the Fed would have to take concrete action to raise inflation to its new target. This would involve lowering interest rates considerably, because inflation would now be about 2.4% below target instead of just 0.4%. A useful way of thinking about this is comparing a Taylor Rule with a 2% inflation target and one with a 4% inflation target.

I know that even the people who signed the letter weren't suggesting an immediate switch to a higher inflation target, but to the extent that they want the change to happen in the next few years, during which the economic climate will probably remain about the same, it's unclear as to whether or not a quick increase in inflation is actually that possible.

No comments:

Post a Comment